Taking part in a blockchain congress was definitely not a thing that I expected to do at some point of my life. Taking part as a lecturer was directly, unthinkable. However, last Wednesday I found myself in front of my laptop, ready to present the work I had been preparing with my team to an audience formed by more than 50 people. But instead of asking myself why was I there, I was truly satisfied to have the opportunity to share something I had been working on (with my teammates, of course) for more than a month.

The logical question now is: how did I get there? Well, everything started when Judit Mendoza, our Banking Management teacher, told us at the beginning of the semester that we would be taking part in a congress related to blockchain and its applications in different economic sectors, including banking and auditing. I would be lying if I told that I was excited at first: my knowledge about blockchain was near to zero and I had never taken part in such a big event before. However, everything changed when we started to work on it.

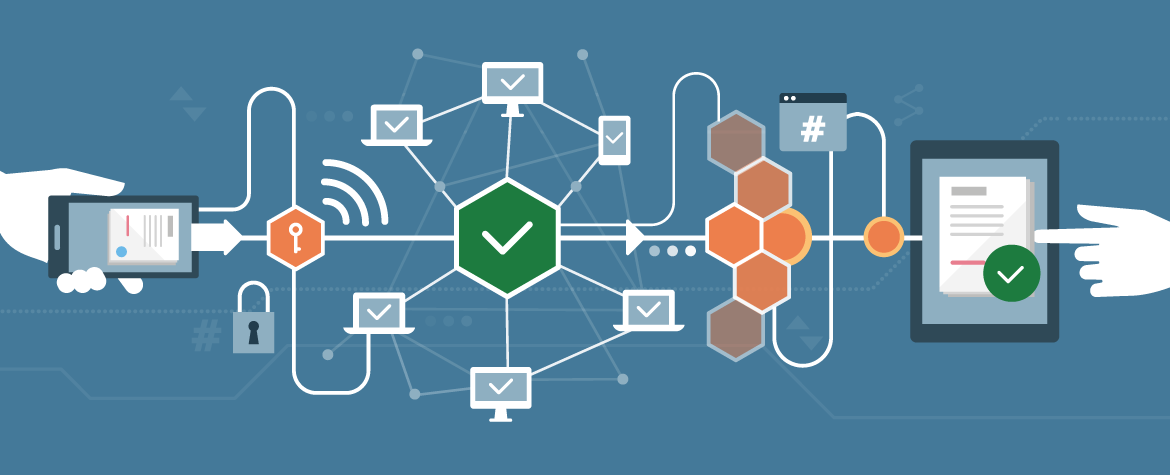

Preparing the academic paper for the congress was almost as thrilling as the congress itself. We chose the risks and benefits of the use of blockchain technology in the banking sector as our topic, and we set some online meetings to prepare the paper. At first it was quite challenging: none of us had written any academic essay before, and it is even more difficult when you must use a language which is not your native tongue. Besides, we had to search a lot of information about blockchain, as we wanted to understand how the technology worked.

Still, as we moved on, we started to enjoy the process. Searching for academic papers published by experts and choosing the right ones for our bibliography gave us a better insight into the fascinating world of scientific publications, and writing the paper was an experience which helped us not only to learn about the disruptive potential of the application of this technology in banking, but also to gain some skills that will definitely be essential for our academic and professional future.

The week before the congress we were already nervous, but also excited. We sent out teacher the final version of our paper and we even corrected the mistakes with the aid of Isabella, an American investigator from Chicago that came to Tenerife as part of the Fulbright programme. Everything was ready for the decisive moment.

We expounded the content of our paper in about seven minutes. I think it went well, or at least we were happy with the outcome. Also, I must admit that I felt rewarded when I answered the questions that some of the other participants asked us, because in that moment I realised about how much I had learned. And that’s the thing: we learned. We learned about blockchain, we learned about its applications in banking, we learned about how to search for academic papers, we learned about how to work efficiently and as a team… That’s why I enjoyed the congress and I appreciated it so much, as it was a unique opportunity to develop some skills that are necessary for our future.

However, the most interesting part were the other participants’ explanations, as they made me realise about the vast amount of possibilities that blockchain technology could offer not only to banking, but also to all kind of activities. We talked about auditing, accounting, and even some participants showed us the apps they created by using this disruptive technology. Personally, I think that the most interesting debate that came up during the congress was the one about if the implementation of blockchain technology could make some jobs redundant. That evidenced the need to adapt the way we work to the new technologies that are dramatically changing the way we live.

In the end, it was an amazing experience and I really hope there will be a second edition next year (hopefully in-person). I can only be thankful to all the participants and organisers for bringing up such an interesting event, even more considering the hard times we are currently living. Definitely, blockchain is the future!